Award-winning PDF software

U.s. tax withholding on payments to foreign persons Form: What You Should Know

W-8BEN — Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding. • IRS Form 5320-X — Certificate of Loss Status of U.S. Person with Respect to Income and Residence Tax with respect to Payments to a Foreign Personal Entity If you sell or trade a non-U.S. citizen to a foreign entity for U.S. source income, that entity is not a United States person (in part because that entity is not a U.S. person (e.g. it is owned or controlled by a foreign corporation)). The entity must, however, have “substantial presence” in the United States because the entity might not be taxed on the income it receives if it received it through a domestic source of income or if the entity is not subject to “loss of U.S. source status.” The United States IRS imposes withholding, tax and penalties on those payments that are not otherwise properly reported to the IRS for U.S. taxes collected. As such, the only way to legally pay a non-U.S. withholding amount on payment of foreign corporation income taxes to a non-U.S. entity is through a tax and penalty-free payment arrangement negotiated between the non-U.S. agent and the foreign tax filing authority (FFL). Such a voluntary scheme is termed a “non-U.S. withholding agreement”. Tax Benefits of Payments To Non-Residents of The United States The “permanent establishment” limitation is eliminated when foreign persons pay foreign corporation (and other) taxable income and use tax-exempt organizations (TEUs) to report and pay their foreign income tax. A non-resident foreign person can establish a permanent establishment in the United States as a result of either bona fide living, working or vacationing in the United States. Therefore, a non-resident foreign person can pay foreign corporation (and other) income to a TEU and use the TEU to report and pay the foreign corporation income tax to the IRS. Payments by a non-resident foreign person to a TEU do not impose on the IRS or TEU a foreign tax credit (Form 5498). Payments to foreign TEUs for the U.S. corporation (and any other taxes that accrue) also do not create a foreign tax credit (Form 3442) or create a U.S.

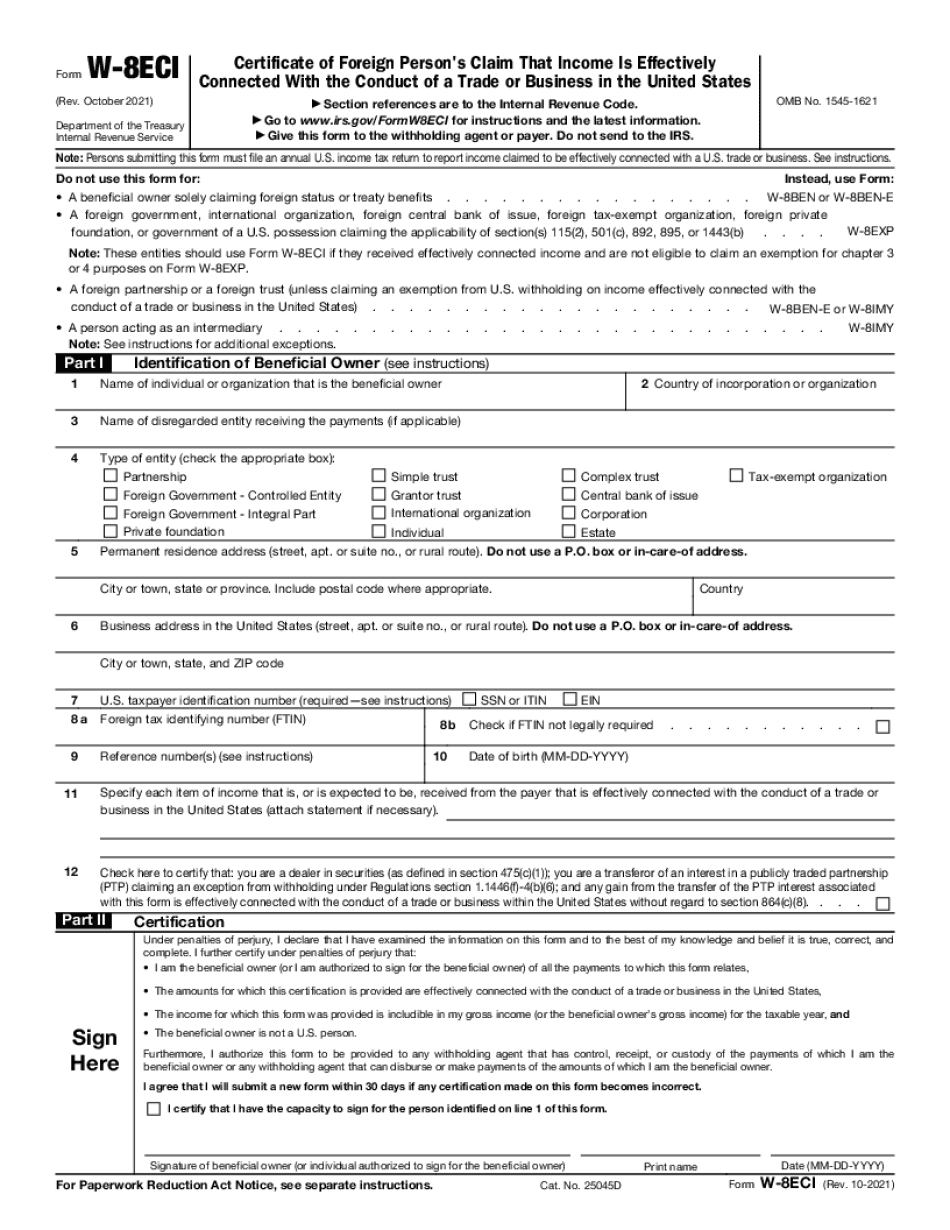

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form W-8eci, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form W-8eci online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form W-8eci by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form W-8eci from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.